How the F#ck to Use Stock Options When Hiring

Many founders ask me… how the f#ck to use stock options when hiring?

When you need a senior hire but don’t have the cash for it, options seem like a natural part of the offer.

But very few founders actually know what they’re getting themselves into.

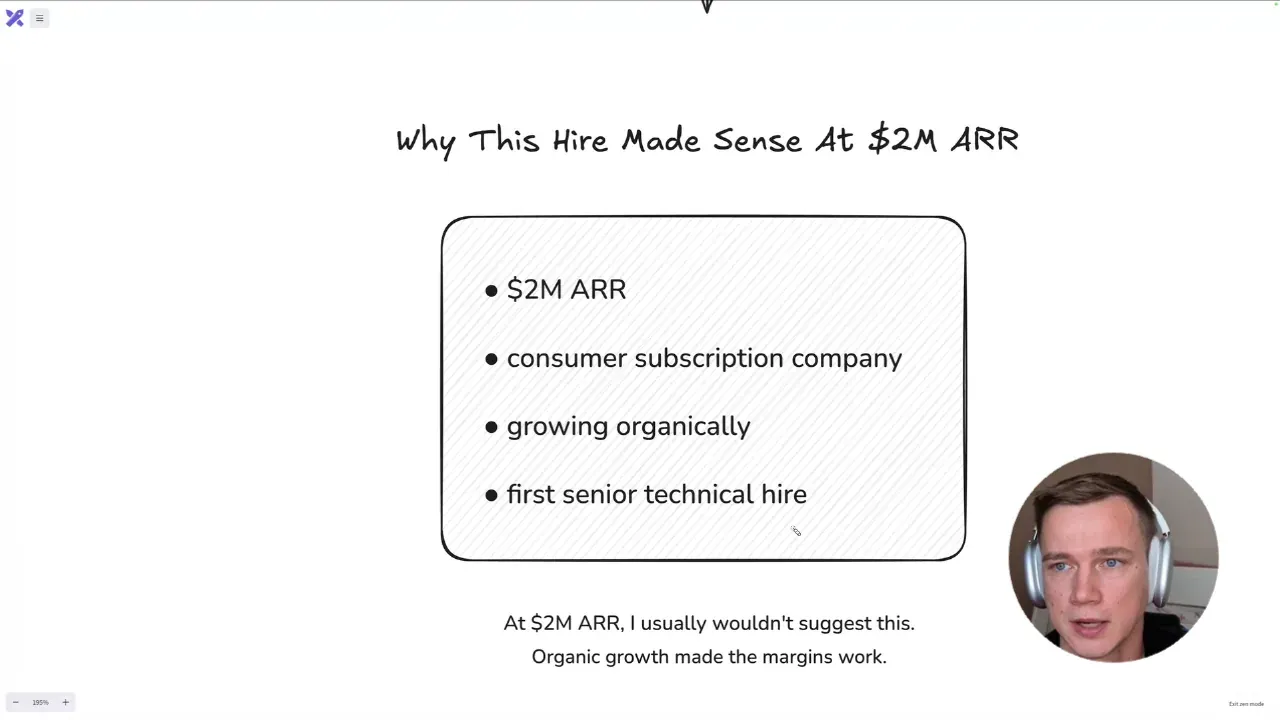

We were helping a consumer subscription company hire their first senior technical person.

Before we get into it, I broke this whole search down on video:

They were around $2M ARR, which is normally early for this kind of hire. But they were growing organically, people loved the product, and margins were strong because they were not buying all the growth through ads. So the hire made sense.

The role started as a Product Engineering Lead.

They did not want a big tech team with separate front-end, back-end, QA, DevOps, designer, and five other people around the product. The product was not that technically complex. They wanted someone who could use AI, keep the team small, and make the product experience much better from the user side.

So the first version of the brief was simple:

- product: 10/10

- tech: strong enough

We found someone who looked like that.

Strong product engineer. Great at understanding product and the user. Product looked great, and tech was around what you would expect from that profile.

But then we realized the real problem.

This person would be the most senior technical person in the company.

So “strong enough technically” was not the same thing as “strong enough to be the most senior tech person.” That changed the whole search.

Then another candidate came in. He was actually CTO-level. He liked the company, the low bureaucracy, the team, and what they were building. He also passed the technical interview properly.

The problem was obvious: he was interviewing elsewhere for CTO-level money.

The company could offer a good base, but not the same cash he could probably get somewhere else. So the rest had to come through upside: stock options, LTIP, or whatever structure they landed on.

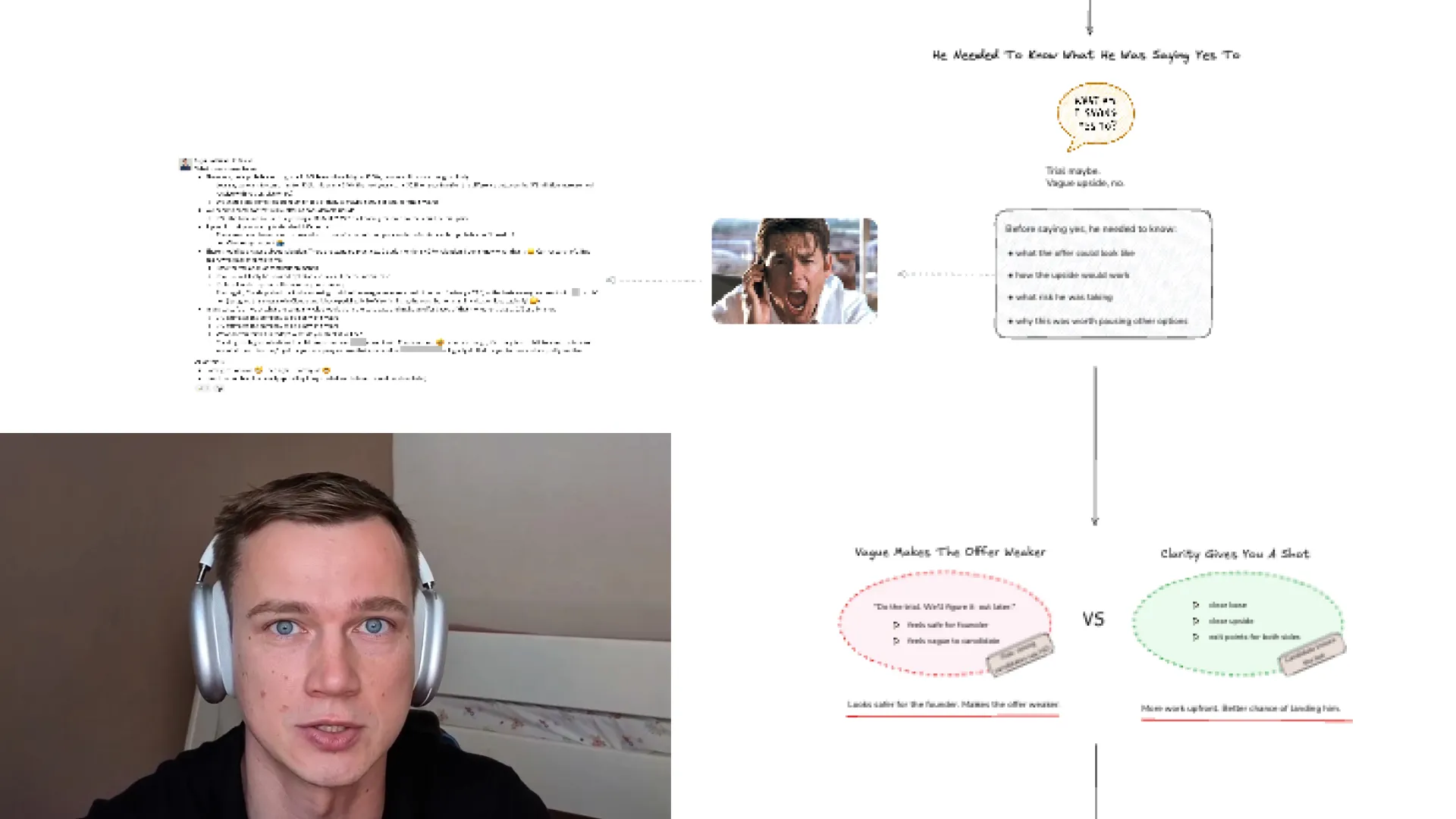

The founder wanted to do a paid trial first and figure out the full package after.

I get why.

You do not want to promise too much before you know if the trial works. You do not want to lock yourself into a bad deal, give away too much equity, or spend weeks building a legal structure for someone who might not be the right person.

That all makes sense from the founder side. But from his side, it sounds like this:

“Come work with us for two weeks and then maybe we will give you an offer you like.”

If I were him, I would probably say no.

The company is fine. I would not know what I am saying yes to.

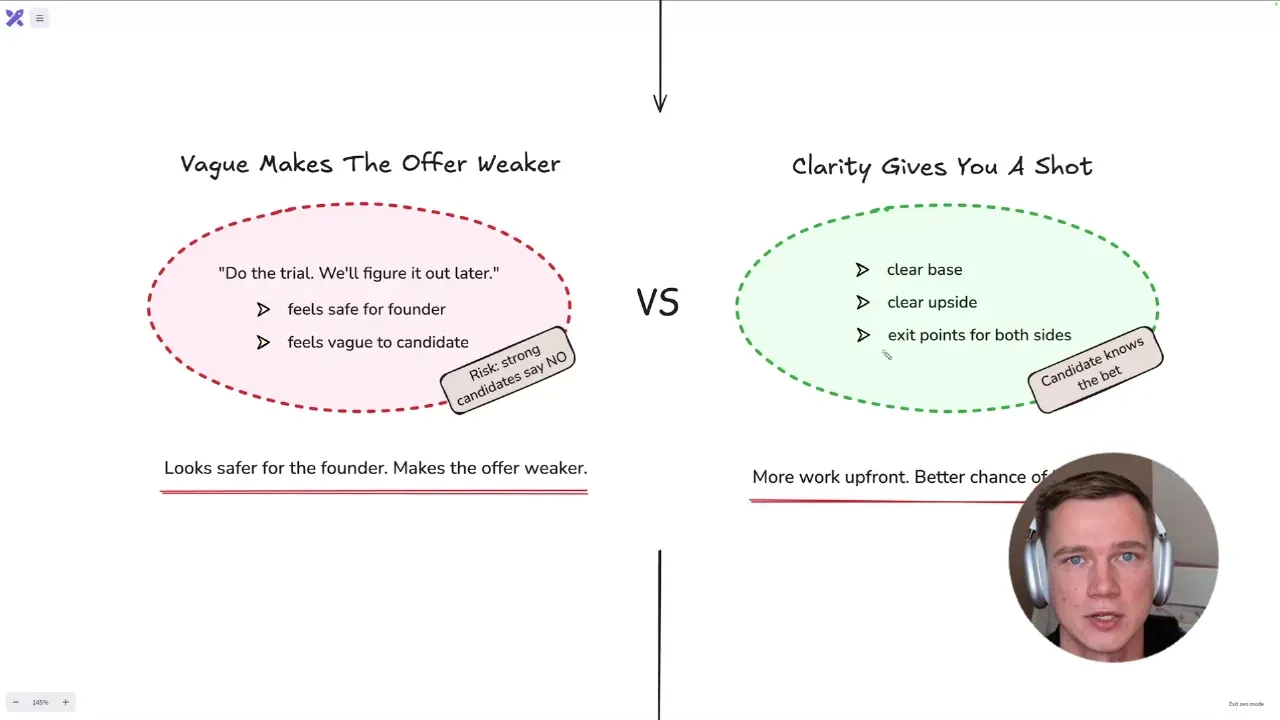

That is the part founders miss.

Keeping your options open can make the offer weaker.

It feels safe because nothing is committed yet, but the best candidates are comparing your opportunity against other real opportunities.

If someone else can explain the role, the cash, the upside, and the path clearly, your vague version loses.

So I pushed back: make the offer real before the trial.

Real enough for him to understand the bet, even before every legal detail was locked:

- base salary

- upside

- what the company would need to be worth for the upside to make sense

- what happens if things go well

- what happens if they do not

- what exit points both sides have if it is not working

That is the difference between playing not to lose and actually trying to win the candidate.

The founder agreed. Her line was simple: two weeks of work for unclear upside is not a great deal. Exactly.

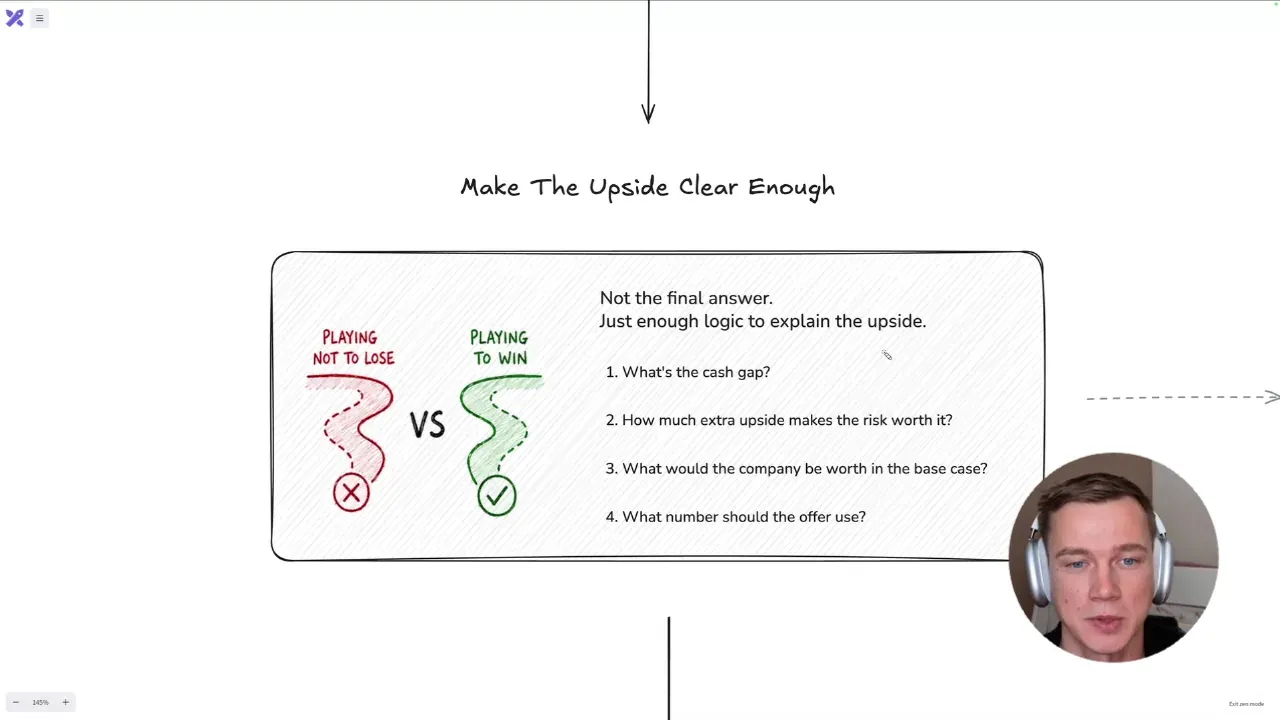

So we built the rough logic. Enough for the founder to explain how she was thinking about the upside, without locking it into a legal document or a final answer.

The questions were:

- What cash is he giving up?

- If he could get more cash somewhere else, what are we making up for?

- What extra upside makes sense because equity is not cash?

- What should the company be worth in the base case?

- Is the offer closer to 1%, 2%, or something else?

- What valuation logic actually makes sense for this business?

That last part mattered a lot.

Revenue was not the cleanest answer here. If they started pushing hard into paid ads, revenue could go up without the business actually getting much better.

Profit was not perfect either.

The founders wanted to pay themselves properly, then reinvest most of the rest back into growth. So profit could underrepresent the value of the company.

So we looked at contribution margin as the cleaner starting point.

Then I told her the important part: this was still some guy’s opinion, not professional valuation advice.

Take the logic, plug in your real numbers, and run it by someone who actually does this.

She took it to an advisor, they generally agreed with the approach, and now they are setting up the LTIP legally.

Instead of telling the candidate “we’ll figure something out,” they are preparing a short overview they can walk him through without setting every detail in stone.

He is starting the trial this week.

That is the main lesson from this search.

This is not really about stock options. It is about candidate psychology.

The best candidates are not only judging your role. They are judging whether you know what kind of person you are trying to hire.

If you want a CTO-level person, do not give them “we’ll figure it out later.”

Make the offer clear enough for them to trust the trial.

The trial was not the problem. The unclear upside was.

Ugis